Episode 2: Natural gas in 2022: from ‘transition fuel’ to ‘last-resort fuel’?

In this second episode of the ultra-mini series on renewable energy post COVID-19, Marcelo Lando, CEO at Eternum Energy, expresses his thoughts on why and how the role of natural gas as “the energy transition fuel” is changing.

The world is now immersed in an unprecedented energy crisis. What was already an extremely volatile environment in late 2021 that had sent spot prices of natural gas to record highs is now (very sadly so) worse with the unjustified invasion to Ukraine by Russia, the country that has the largest proven natural gas reserves in the world.

This recent crisis will have profound implications on the role of natural gas in electricity markets and will fuel two already accelerating trends that provide guidance on how and when the role of natural gas might get redefined. The first trend is the growing uncertainty around climate change. The second is the acceleration of technology and innovation in the renewable energy ecosystem.

This second episode on renewable energy post COVID-19 will provide a brief framework for rethinking about one of the most widely accepted hypotheses in electricity markets: that natural gas will provide a decades-long bridge to a future powered by renewable energy.

Spoiler Alert: the natural gas bridge might be shorter and narrower than previously anticipated as natural gas becomes less and less competitive in electricity markets.

Trend #1: Technology and innovations in the renewable energy ecosystem are leaving less room for natural gas

Innovation and technology in the renewable energy ecosystem typically come in three forms: (i) technological improvements in hardware, (ii) improvements in forecasting solar & wind generation, and (iii) digitalization & advanced software management. A good example of hardware improvements is bifacial solar panels (i.e. panels that can capture solar radiation from both sides of the panel). This step-change in hardware has become the industry standard, providing between a 5 and 15 percent increase in energy yields with a relatively minor increase in capex. Another hardware improvement is floating wind turbines, which have the potential to open-up huge maritime locations for wind farms that were not previously economical.

Figure 1: Classifying new technology and innovations in the renewable energy ecosystem.

Trend #2: The uncertainty around climate change is increasingly expanding beyond carbon pricing

One of the advantages of financial markets is that scenarios of future costs are brought to present value. In the case of gas power plants in operation, decisions are less critical since the investment has already been made. However, when considering to either develop a new gas power plant or acquire an existing one, future scenarios, and their corresponding cash flows, define if the investment goes forward or not. For power plants, this is important because cash flows are typically modelled for more than 20 years in line with the life of the underlying asset.

Back in 2010, when we prepared financial models to make investment decisions on the acquisition or development of gas power plants, we rarely considered a price for greenhouse gas (“GHG”) emissions – with the exception of projects in the European Union. For the full twenty or twenty-five years of the projections, the cost assumed for GHG emissions, including CO2 emissions, was zero. Sometimes financial models estimated a price for CO2 but later canceled that cost by assuming enough free allowances to cover all MWh – which brings us back to the earlier case.

Fast forward to today and all projections include some form of cost associated to GHG emissions, especially CO2 emissions – be it a carbon tax, a carbon price, or other costs directly associated to potential future GHG regulations. Since lenders provide leverage according to the size of annual expected cash flows, a future cost on emissions reduces the leverage, and this in turn reduces the return to the equity investors. Gas power plants emit roughly 500 kg of CO2 per MWh, which is approximately half of the CO2 per MWh compared to a coal power plant (and not considering methane leaks which EIA just reported are much higher than expected). In Europe, the cost associated with one MWh of a gas power plant would be approximately 40 to 45 euros. This variable emissions cost makes new gas power plants in Europe a challenging investment, with a few exceptions where gas power plants are designed to run short periods of time at very high prices.

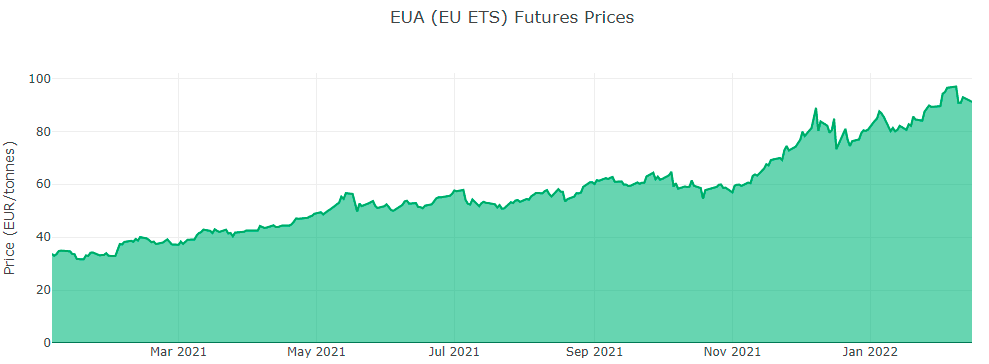

Figure 2: The price of CO2 emission allowances in the European Union (“EUA”) have sky-rocketed to over 90 EUR per CO2 ton (source: Ember). Each EUA allowance gives the right to emit one ton of carbon dioxide equivalent in the European Union, UK, Norway, Iceland or Liechtenstein.

However, a future price on carbon is just one side of the problem related to expected cash flows. As climate change becomes a higher priority around the world, the uncertainty associated with carbon intensive industries increases[1]. For example, insurance giant AON estimated losses attributed to climate events in 2021 were $329 billion, the third costliest year on record. If climate events continue to increase in severity, how could the reaction of governments, and society in general, impact emissions intensive industries such as gas power plants?.

Most of the time, investors and banks will incorporate this climate change uncertainty into the decision-making process by either increasing the future cost of carbon or by increasing the interest rate of the financing. To what degree does the combination of CO2 cost and uncertainty around climate change make new gas-power plants uneconomical? It all comes down to the assumptions that investors and banks make on (i) the costs associated to emissions, (ii) the timing of when that cost is set to kick-in, (iii) the rate at which this cost is set to increase thereafter, and (iv) the possibility (or lack thereof) for carbon capture to become an economic reality.

The three key growth areas of natural gas as a “transition” fuel that are being challenged

Regulators around the world have traditionally thought of natural gas as a source of electricity in three main cases:

a) As a replacement of coal, which still powers about 35% of worldwide electricity demand. However, consider the case of Chile, the third largest electricity market in South America after Brazil and Argentina. From 2016 to 2021 the share of solar & wind increased from 7% to 22%, while the share of coal went from 44% to 34%. Natural gas increased its share by only 1%[2]. Other electricity markets trying to make similar changes have the additional advantage of experience and continued cost reductions in technology.

b) To meet the growth in electricity demand which is expected to increase globally by about 3% per year, from about 27.000 TWh today to 35.000 GWh in 2030 according to DNV´s Energy Transition Outlook[3]. This increase in demand will be mostly concentrated in China and India where the increase demand for natural gas will have to come from imports. A recent report from the IEA[4] expects that 90% of the increase in electricity demand will be served by renewables – let us just remember that IEA has historically been underestimating the growth of solar and wind as did most analysts.

c) To fill intra-day gaps once solar and wind achieve a significant share of the electricity mix. This has been the area where solar and wind get the most pushback, particularly from legacy energy players. However, most of the electricity markets around the world are not yet facing these challenges and can still grow their solar & wind share without worrying much about intra-day variations. In addition, the sudden drop in electricity demand that followed the COVID-19 lockdowns forced grid operators to handle shares of solar & wind that were previously unthought of – and they did just fine[5]. At what share of solar & wind penetration does intra-day imbalances begin to affect the grid? While this varies with the ability of the grid to manage imbalances (e.g., ability to export and import electricity, ability to use hydropower as a buffer, among other factors), the figure below could help provide some insights depending on the share of solar & wind, from the “Initiation” stage to the “Pioneering” stage.

What to monitor next?

To what extent will natural gas get squeezed out as a “transition” fuel in electricity markets? Capital & talent continue to feed the technology & innovation trend. In parallel, a derailed path to the 1.5-degree Celsius world will further feed the climate change uncertainty. As pressure mounts and as energy security becomes a crucial priority, what the world will now monitor is the reaction from politicians and regulators at a global & local level. That will be the subject of Episode 3 of the mini series of renewable energy post COVID-19.

Note: This is the second episode of the ultra-mini-series on renewable energy post COVID-19. The next episode will provide insights to smart regulation – the lowest hanging fruit to assist the energy transition.

Opinions in this article are entirely my own. However, many professionals from diverse industries have generously contributed with their feedback to an earlier draft. I want to especially thank the always insightful comments from Björn Ullbro, Don Green and Francesco Venturini.

[1] A very insightful paper on uncertainty associated with climate change was written by Mike Barnett, William Brock and Lars Peter Hansen although their focus was on uncertainty as seen by a policy maker rather than by an investor “Confronting Uncertainty in the Climate Change Dynamics”.

[2] Historical Generation by Technology (Coordinador Eléctrico Nacional de Chile).

[3] A very valuable Full Report is available here. The expected growth in demand also accounts for the increased electrification of the economy and subtracts the expected increased efficiency.

[4] Electricity Market Report (IEA, 2022), full report available here.